Quick Guide to Medigap Plans

In Triage Health's free Quick Guide to Medigap Plans, you'll learn about the parts of Medicare, how to qualify for Medigap, when to buy a Medigap plan, and differences by state.

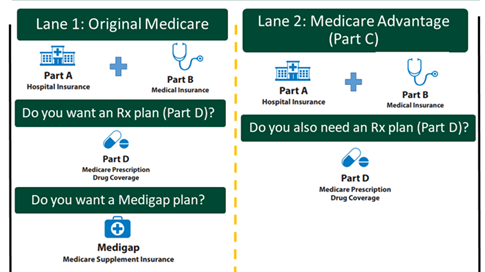

Medicare is a government-funded and run health insurance program. To be eligible for Medicare, you must: be 65+ years old; have collected SSDI more than 24 months; or have been diagnosed with end-stage renal disease (ESRD) or ALS. Medicare coverage is broken down into 4 parts:

- Part A: Hospital Insurance. Includes hospital care, skilled nursing facilities, nursing homes, hospice, & home health.

- Part B: Medical Insurance. Includes outpatient services, preventive care, labs, mental health care, ambulances, & durable medical equipment.

- Part D: Prescription Drug Coverage. You have different plans to choose from depending on where you live, with different premiums and formularies.

- Part C: Advantage Plans. Part C is an alternative to Parts A & B and includes the benefits and services covered under Parts A & B, and usually Part D. You can select a PPO or HMO plan that is run by a Medicare-approved private insurance company. If you buy a Part C plan, you are not eligible to buy a Medigap plan.

How do I qualify for Medigap?

Medigap plans are additional insurance you can purchase to help pay deductibles, co-payments, co-insurance amounts, and other expenses original Medicare does not cover. You can buy a Medigap policy from any licensed insurance company in your state. You will pay an additional monthly premium for a Medigap plan, in addition to premiums for other Medicare parts. Medigap plans are standardized, meaning every insurer offers plans lettered A-N.

| Coverage | Plan A | Plan B | Plan C | Plan D | Plan F | Plan G | Plan K | Plan L | Plan M | Plan N |

|---|---|---|---|---|---|---|---|---|---|---|

| Medicare Part A Co-insurance & Hospital Costs (Up to an additional 365 days after Medicare benefits are used) | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% |

| Medicare Part B Co-insurance or Co-payments | 100% | 100% | 100% | 100% | 100% | 100% | 50% | 75% | 100% | 100% |

| Blood First 3 Pints | 100% | 100% | 100% | 100% | 100% | 100% | 50% | 75% | 100% | 100% |

| Part A Hospice Co-insurance or Co-payments | 100% | 100% | 100% | 100% | 100% | 100% | 50% | 75% | 100% | 100% |

| Skilled Nursing Facility Co-insurance | x | x | 100% | 100% | 100% | 100% | 50% | 75% | 100% | 100% |

| Medicare Part A Deducible | x | 100% | 100% | 100% | 100% | 100% | 50% | 75% | 50% | 100% |

| Medicare Part B Deductible | x | x | 100% | x | 100% | x | x | x | x | x |

| Medicare Part B Excess Charges | x | x | x | x | 100% | 100% | x | x | x | x |

| Foreign Travel Emergency (up to plan limits) | x | x | 80% | 80% | 80% | 80% | x | x | 80% | 80% |

| Out of Pocket Maximum | $8,000 in 2026 | $4,000 in 2026 |

The percentage shown is the amount the Medigap plan covers.

To qualify for a Medigap plan, you must be enrolled in Medicare Part A and B. Part A and B together are referred to as “Original Medicare.” For a more in-depth breakdown of Medicare Parts A and B, see our Quick Guide to Medicare – Extended.

When Should I Buy a Medigap Plan?

The best time to purchase a Medigap plan is during your Medigap Open Enrollment Period. This is the 6-months that begin the first day of the month you are 65 or older and you have signed up for Part B. If you enroll in a Medigap plan during this period of time, you cannot be denied coverage.

If you wait to buy a plan outside of your Medigap Open Enrollment Period, and you do not have a “guaranteed issue right,” you may face a pre-existing condition exclusion period of up to 6-months, the plan may cost more, and/or you may be denied coverage. “Guaranteed Issue Rights” exist in certain limited situations (e.g., your Medicare Advantage plan is leaving Medicare or you move out of the plan’s service area). For a list of these situations, visit Medicare.gov/health-drug-plans-/medigap/ready-to-buy. Some states provide additional guaranteed issue rights.

Once you have a Medigap plan, it is automatically eligible for renewal, regardless of any health problems. Your Medigap plan can only be canceled if you fail to pay the premiums.

If you are under 65, and have Medicare because of a disability, your state may not require insurance companies to sell you a Medigap plan. Visit TriageHealth.org/state-laws for more information.

Example

Part B of Medicare has a 20% co-insurance amount. Most chemotherapies are covered under Medicare Part B, which can create high out-of-pocket costs. Buying a Medigap plan that covers Part B’s 20% co-insurance can greatly reduce your out-of-pocket costs. These examples show how:

- Jimmy: Jimmy is nearly 65, lives in Chicago, and is about to begin 1 year of IV chemotherapy treatments, which will cost $10,000 a month. What would be his out-of-pocket costs?

- Option 1: Original Medicare

- Part B monthly premium = $202.90 per month x 12 = $2,434.80

- Part B deductible = $283

- Part B co-insurance (just for his chemo) = $10,000 x 20% = $2,000 x 12 months = $24,000

- Total for Part B and chemo cost-share = $27,717.80

- Option 2: Original Medicare + Medigap Plan G, which costs $300/month based on his age and where he lives

- Part B monthly premium = $202.90 per month x 12 = $2,434.80

- Part B deductible = $283

- Part B co-insurance (just for his chemo) = $0 (paid for by Medigap plan)

- Medigap Plan G monthly premium = $300 x 12 months = $3,600

- Total for Part B and Medigap Plan G = $6,317.80

- Jimmy: Even if Jimmy did not sign up during his IEP and faces a 6-month pre-existing condition exclusion period for anything related to his cancer, a Medigap plan could still save him money:

- Original Medicare + Medigap Plan G, with a 6-month exclusion period

- Part B monthly premium = $202.90 per month x 12 = $2,434.80

- Part B deductible = $283

- Part B co-insurance (just for first 6 months of chemo) = $10,000 x 20% = $2,000 x 6 months = $12,000

- Part B co-insurance (just for second 6 months of chemo) = $0 (paid for by Medigap plan)

- Medigap Plan G monthly premium = $300 x 12 months = $3,600

- Total for Part B and Medigap Plan G = $18,317.80

- Original Medicare + Medigap Plan G, with a 6-month exclusion period

- Option 1: Original Medicare

Differences by State

If you live in Massachusetts, Minnesota, or Wisconsin, Medigap policies are standardized in a different way. For more information visit medicare.gov/health-drug-plans/medigap/basics.

Learn More

For more information visit our Health Insurance and Medicare resource pages.

Sharing Our Quick Guides

We're glad you found this resource helpful! Please feel free to share this resource with your communities or to post a link on your organization's website. If you are a health care professional, we provide free, bulk copies of many of our resources. To make a request, visit TriageHealth.org/MaterialRequest.

However, this content may not be reproduced, in whole or in part, without the express permission of Triage Cancer. Please email us at TriageHealth@TriageCancer.org to request permission.

Last reviewed for updates: 1/2026

Disclaimer: This handout is intended to provide general information on the topics presented. It is provided with the understanding that Triage Cancer is not engaged in rendering any legal, medical, or professional services by its publication or distribution. Although this content was reviewed by a professional, it should not be used as a substitute for professional services. © Triage Cancer 2026