What is a Co-Pay Maximizer Program?

A co-pay maximizer works differently than a co-pay accumulator. Instead of applying the financial assistance first, until it runs out, the insurance company will spread the total amount of the copay assistance across the plan year.

Example:

- Maya’s prescription’s out-of-pocket costs: $1,200/month

- Maya’s plan’s out-of-pocket maximum: $6,000/year

- Co-pay assistance amount: $12,000/total for the year

With a Co-Pay Maximizer

With a maximizer, the plan changes her out-of-pocket cost to match the total co-pay assistance available and spreads it out across the full year.

This means Maya would pay $0 out-of-pocket for her prescription, but does not make progress toward reaching the out-of-pocket maximum and will have to pay her out-of-pocket costs for other health care she receives.

Without a Co-Pay Maximizer

Assistance is used up by October. Maya may owe $1,200 in November and $1,200 in December, if she has not met her out-of-pocket maximum with other health care expenses during the year.

*Whether the co-pay assistance counts toward the out-of-pocket maximum depends on if her plan is also using a co-pay accumulator.

Are Co-pay Accumulators and Maximizers Allowed?

It depends on where you live and the type of health insurance plan you have.

Federal Rules

- Federal regulations currently allow health plans to use accumulator and maximizer programs, except when the medication does not have a generic equivalent.

- Federal rules have changed several times in recent years, so this is an evolving issue.

State Laws

- As of 2026, more than 25 states have passed laws that ban or limit co-pay accumulator programs. Visit: TriageHealth.org/StateLaws for more information.

- Note: these state laws only apply to fully insured plans (e.g., Marketplace plans, insured employer plans). These state laws do not apply to self-insured employer plans.

What Is a Self-Insured Plan?

- Self-insured (or self-funded) health plan: the employer pays for employees’ medical claims directly, instead of buying a policy from an insurance company.

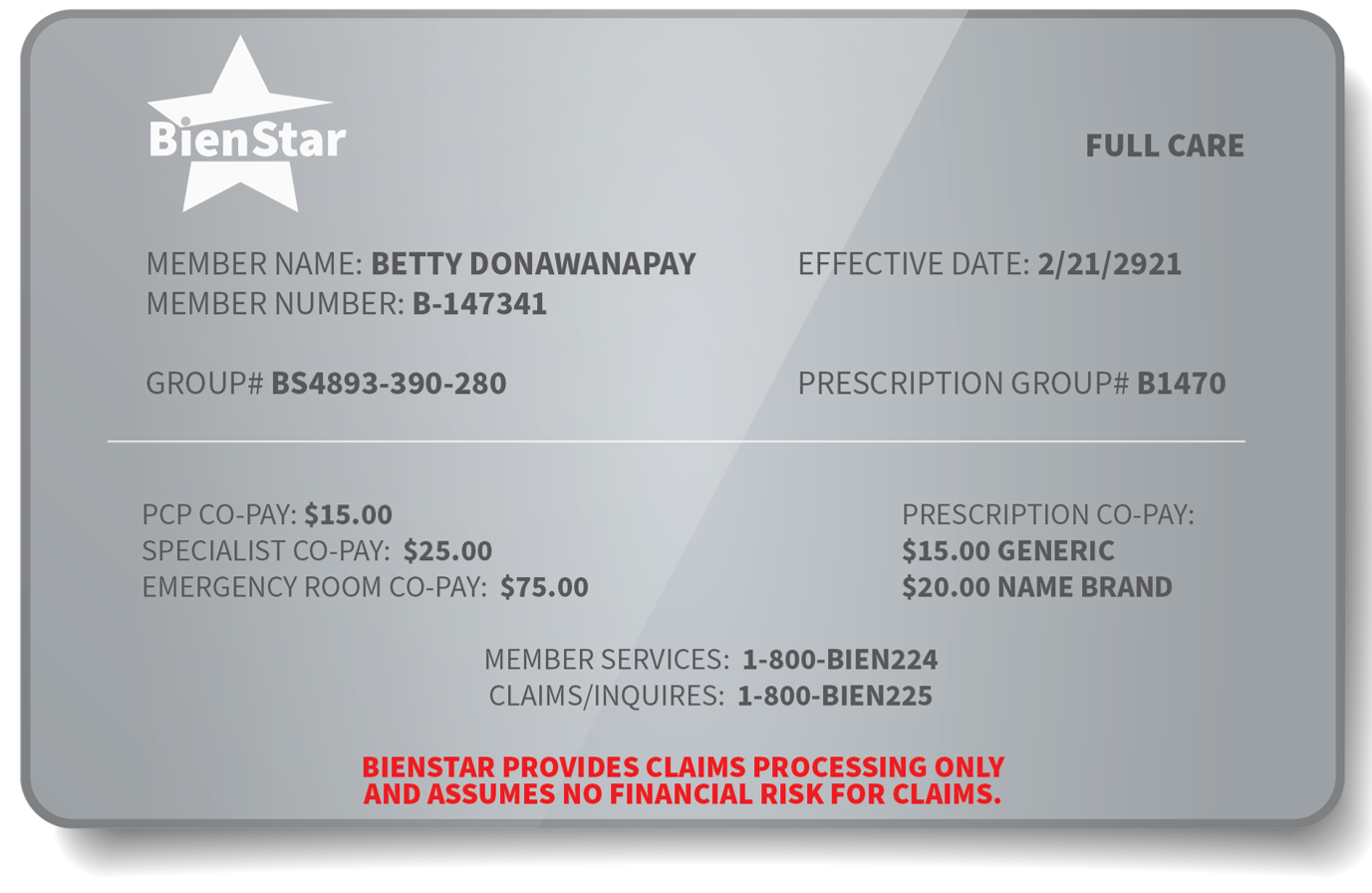

- A third-party administrator (TPA), may administer benefits, process claims, and manage the prescription drug benefit for the employer. That can be confusing because those TPAs are often insurance companies and an employee may have an insurance card with the logo of an insurance company, but it is the employer that is assuming the cost of claims. See this s

ample insurance card with self-insured language in red.

ample insurance card with self-insured language in red.

How to Tell If Your Plan Is Self-Insured?

- Review your plan documents, including the Summary Plan Description (SPD). It may state whether the plan is “self-insured” or “self-funded.”

- Ask your HR or benefits administrator: “Is our group health plan self-insured?”

- Statements in plan materials like “ERISA plan,” “self-insured employer plan,” or “providing claims processing only,” are clues that you have a self-insured plan.

How to Find Out if Your Plan Uses These Programs?

- Review your Summary of Benefits and Coverage (SBC) or your Plan Documents (also called Evidence of Coverage).

- Look for terms like “co-pay accumulator adjustment,” “co-pay offset program,” “co-pay maximizer,” “coupon adjustment,” “co-pay leveling program,” “benefit plan protection program,” or “out-of-pocket protection program.”

- Contact your insurance company’s member services and ask directly: “Does my plan have a co-pay accumulator or maximizer program that affects co-pay assistance?”

- If your coverage is through your employer, ask your HR or benefits administrator whether your plan includes one of these programs.

- It is also important to ask if using these programs is required by your employer-sponsored plan. In some cases, you may be able to opt out, if you ask.